ACMR, ACM Research: Riding China’s Domestic-First Chip Boom

ACM Research builds wafer cleaning, plating, furnace, and track tools for semiconductor fabs. The company reported $215.4 million in revenue for Q2 2025. Most shipments and tool acceptances are tied to mainland China customers.

Latest News

On September 7, 2025, ACM shipped its first high-throughput Ultra Lith KrF track system to a leading logic fab in China. This marked an expansion beyond cleaning into coater-developer tracks. The product is a 300 WPH KrF track, with a revenue model combining capital sales, spares, and service.

Later, on September 29, 2025, ACM Shanghai reported a backlog of RMB 9.07 billion, up 34.1 percent year over year. This figure includes shipped tools not yet recognized as revenue and future orders. These developments are significant because track tools expand ACM’s wallet share and process coverage, while the growing China-heavy backlog highlights durable domestic demand and ongoing localization momentum.

Recent Earnings

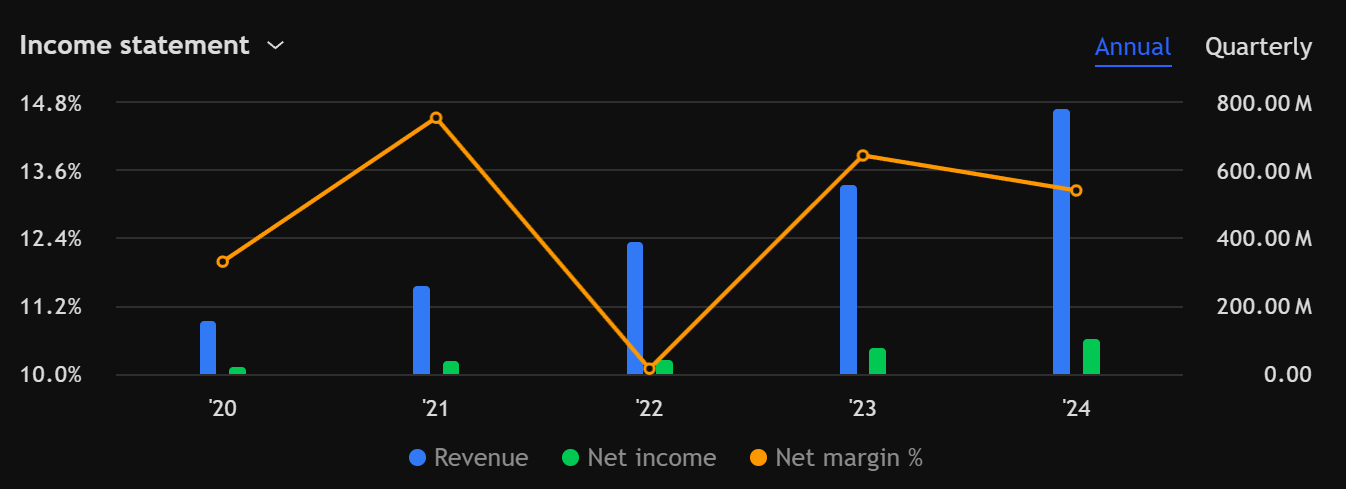

For Q2 2025, which ended on June 30 and was reported on August 6, ACM recorded $215.4 million in revenue, a 6.4 percent increase from the prior year. Gross margin was approximately 48.5 percent, and GAAP operating income reached $31.7 million. Cash and time deposits stood at $483.9 million. Earnings per share exceeded expectations, while revenue came in slightly below consensus due to shipment timing and revenue recognition typical in China. Full-year 2025 guidance remained at $850 to $950 million.

During the August 6 management call, CEO David Wang emphasized continued strength in single-wafer cleaning, Tahoe semi-critical clean, plating, and furnace segments. He reaffirmed confidence in 2025 performance and highlighted ongoing product expansion into tracks. The overall message was steady growth, strong profitability, and a balance sheet positioned to support more installations and service coverage.

Analysis and Forward Outlook

ACM’s momentum in China stems from both favorable policy conditions and effective local execution.

First, domestic policy and procurement preferences favor local suppliers in mature and semi-critical process nodes. China’s accelerated effort to localize semiconductor inputs in 2025 has improved win rates for capable local vendors. In cleaning and track systems, where uptime, reliability, and service proximity are critical, ACM’s established presence gives it a clear advantage.

Second, the company continues to expand its product lineup to cover more fabrication steps. The September KrF track delivery opens a new front near lithography, complementing its large installed base of single-wafer and Tahoe cleaners. Once a tool becomes process of record, recurring spares, upgrades, and follow-on sales compound over time. The late-September backlog growth reflects this expanding process footprint.

Third, ACM Shanghai’s private offering in late September raised roughly RMB 4.5 billion to fund R&D and capital expenditures. This move strengthens ACM’s onshore operations and aligns with customer preferences for locally funded and staffed suppliers. Localized operations shorten qualification cycles and reduce geopolitical friction in procurement.

However, risks remain. U.S. and allied export controls continue to evolve, and Beijing has introduced new restrictions on critical inputs. A slowdown in capital spending by Chinese logic or memory customers would directly impact orders and tool acceptances. Even so, ACM’s diversified product mix now spans more process steps per wafer, and its large installed base supports recurring service revenue that can cushion softer order periods.

Conclusion

ACM appears to be China’s preferred domestic supplier for wafer cleaning and track systems. The company’s expanding backlog, new product platforms, and strong local capital base reinforce its position in the Chinese semiconductor ecosystem. If the success of its track systems extends across more fabs while cleaning tools maintain share, ACM’s 2025 guidance looks attainable. Despite policy uncertainty, its China-centered growth story remains solid and sustainable.

Bullish outlook

ACMR 0.00%↑

Disclaimer:

All views expressed are my own and are provided solely for informational and educational purposes. This is not investment, legal, tax, or accounting advice, nor a recommendation to buy or sell any security. While I aim for accuracy, I cannot guarantee completeness or timeliness of information. The strategies and securities discussed may not suit every investor; past performance does not predict future results, and all investments carry risk, including loss of principal.

I may hold, or have held, positions in any mentioned securities. Opinions herein are subject to change without notice. This material reflects my personal views and does not represent those of any employer or affiliated organization. Please conduct your own research and consult a licensed professional before making any investment decisions.