AMD, Advanced Micro Devices: OpenAI’s Software Gravity Can Turbocharge ROCm and Close the CUDA Gap

AMD ROCm vs CUDA, AI Data Center GPUs

Advanced Micro Devices is the second-largest supplier of data center silicon. Its Instinct accelerators already power multi-vendor AI clusters. With OpenAI as a marquee customer, the key question is how quickly software can unlock the hardware.

Latest News

On October 6, 2025, AMD and OpenAI announced a multi-year, multi-generation agreement to deploy up to 6 gigawatts of AMD GPU capacity. The rollout will begin in 2026 with an initial 1 gigawatt of Instinct MI450 systems in the United States. Under the deal, OpenAI will receive share options tied to specific milestones.

The revenue model combines long-term supply commitments, potential equity incentives, and large follow-on clusters that scale with model demand. This partnership transforms AMD from a backup supplier into a design-center partner, integrating ROCm deeply into OpenAI’s daily training and inference workflows.

The market reaction was immediate. Analysts described the deal as “blockbuster,” while others noted that execution, rather than headlines, will determine the ultimate value creation.

Recent Earnings

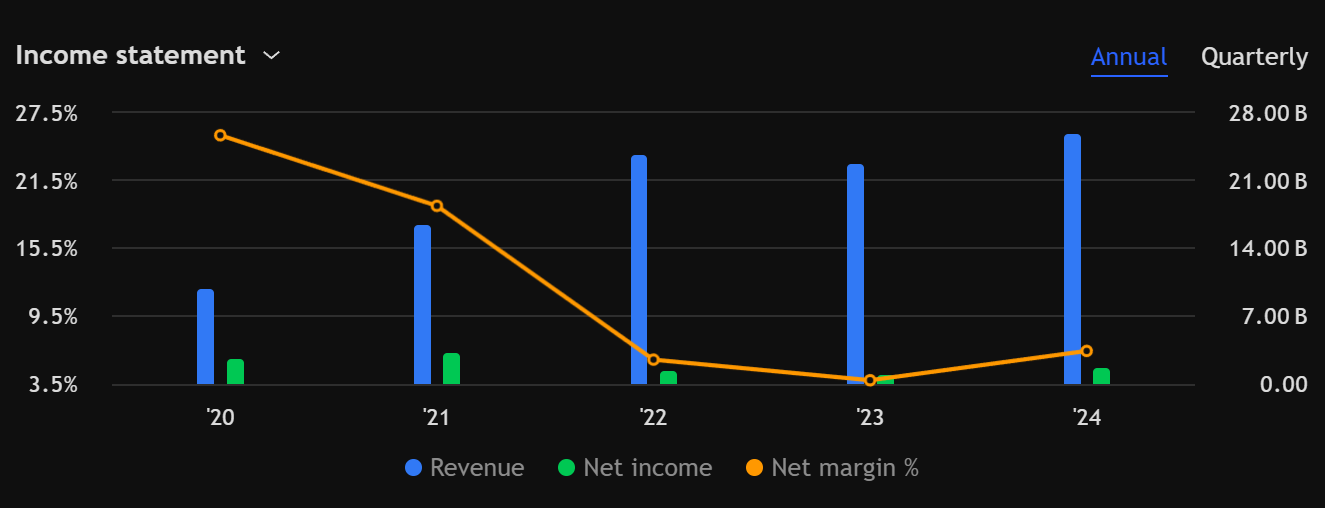

AMD’s most recent quarter was Q2 2025, which ended June 28 and was released on August 5. Revenue grew 32 percent year over year to $7.69 billion. Non-GAAP operating income was $897 million, adjusted EBITDA reached $1.09 billion, and free cash flow totaled $1.18 billion, supported by $5.87 billion in cash and short-term investments. GAAP operating income was negative due to an $800 million inventory charge tied to export restrictions.

Results came in above the midpoint of guidance and surpassed several revenue estimates. Management credited strong EPYC and Ryzen sales, while Instinct performance was constrained by China license issues, which were excluded from forward guidance.

CEO Lisa Su said the company is positioned for “robust future growth,” and CFO Jean Hu emphasized record free cash flow despite the inventory charge. The outlook for Q3 called for approximately $8.7 billion in revenue, driven by the MI350 ramp.

Analysis and Forward Outlook

The OpenAI partnership is more than a supply deal; it is a catalyst for software acceleration. If OpenAI engineers optimize PyTorch pathways, compiler stacks, and kernels for ROCm 7 and beyond, the cumulative effect of those daily improvements could narrow the performance gap that has long favored Nvidia.

ROCm’s open-source model encourages upstream collaboration. OpenAI’s engineering teams are pragmatic about throughput and stability and are expected to stress-test ROCm across FP4 inference, distributed training, and large-scale frontier workloads. The outcome will be portable recipes, reproducible containers, and publicly available fixes that cloud providers can readily adopt.

AMD stands to benefit twice: first, by absorbing OpenAI’s software advancements directly into ROCm, and second, by allowing OEMs and hyperscalers to reuse those optimizations across MI350 and MI450 platforms. The equity-linked structure further aligns incentives for shared road mapping and tight integration of hardware, firmware, and software development.

If the 6-gigawatt buildout proceeds as planned and ROCm achieves performance parity on key models, consensus forecasts for revenue and margins are likely to rise. AMD’s AI story would shift from one limited by capacity to one driven by software credibility. Execution risk remains, but the upside is substantial if OpenAI’s software momentum centers on ROCm.

Conclusion

I remain bullish. The OpenAI partnership channels world-class software expertise directly into ROCm, which is precisely what AMD needed. If deployment stays on schedule and ROCm continues to close the performance gap, AMD has a credible path to reach $600 per share over the next cycle, with software innovation contributing as much as hardware capacity.

Bullish outlook

Disclaimer:

“All views expressed are my own and are provided solely for informational and educational purposes. This is not investment, legal, tax, or accounting advice, nor a recommendation to buy or sell any security. While I aim for accuracy, I cannot guarantee completeness or timeliness of information. The strategies and securities discussed may not suit every investor; past performance does not predict future results, and all investments carry risk, including loss of principal.

I may hold, or have held, positions in any mentioned securities. Opinions herein are subject to change without notice. This material reflects my personal views and does not represent those of any employer or affiliated organization. Please conduct your own research and consult a licensed professional before making any investment decisions.”