$QCOM: Qualcomm, The AI Semiconductor Late Bloomer Wall Street Missed

QCOM stock analysis 2026, Qualcomm edge AI investment thesis, undervalued AI chip stocks, Qualcomm data center ASIC

Investors who correctly identified the artificial intelligence boom often face a unique frustration. Many bought into the right sector but chose the wrong stock. Those who held Qualcomm stock over the past two years while Nvidia, Broadcom, and AMD delivered massive gains know this feeling well. The early semiconductor trade left Qualcomm behind. That dynamic is now shifting.

On May 26, 2026, Qualcomm stock reached an all-time closing high of $248.82. Shares surged as much as 8% during the trading session following a major Bloomberg report. The company secured a landmark deal to supply millions of AI chips to ByteDance, the parent company of TikTok and a massive buyer of AI infrastructure. This agreement covers application-specific integrated circuits, or ASICs, designed for the ByteDance Doubao chatbot and AI agent software. It provides undeniable commercial validation. Qualcomm spent eighteen months building a data center business. The company now has a major enterprise customer to prove its progress.

The Dual Growth Engines: Edge AI and Data Centers

For years, consumers and financial markets defined Qualcomm by the Snapdragon mobile processors inside Android smartphones. That view is no longer complete. The company is actively participating in two major technology shifts. The broader market is just beginning to price in these changes.

The first shift is edge computing. Processing power is moving away from remote cloud servers. Devices now handle artificial intelligence locally on your phone, inside your car, or at your desk. Arm-based AI personal computers are projected to capture roughly 30% of the total PC market by the end of 2026. That is a steep climb from just 13% in 2025. Qualcomm launched the Snapdragon X2 Elite at CES 2026 to capture this demand. The 3-nanometer chip delivers 80 TOPS of neural processing performance. It outperforms the Intel Panther Lake processor in AI inference benchmarks while using 43% less power. Industry analysts note Qualcomm holds a 40% to 50% performance-per-watt advantage for ultra-portable computers. Competitors like Intel and AMD cannot easily close that efficiency gap.

CEO Cristiano Amon highlighted this scale during the Q2 FY2026 earnings call. He stated that no other semiconductor company matches their product breadth. Qualcomm hardware powers everything from smart wearables using milliwatts to data centers requiring kilowatts. This reach is driving a massive increase in strategic customer engagement.

The second technology shift involves the data center. Qualcomm acquired Alphawave Semi and Ventana Micro Systems to build a highly competitive data center CPU and AI inference accelerator platform. Management confirmed that initial shipments for an unnamed leading hyperscale cloud provider will begin in December 2026. The ByteDance agreement provides a second major enterprise anchor before those hyperscaler units even ship. Amon noted that the Alphawave integration is advancing well. The company is actively pursuing opportunities with large cloud service providers and sovereign AI projects globally.

Expanding Edge AI: Robotics, Wearables, and Smart Glasses

We are entering a period where almost every consumer and industrial product requires a processor. Smartphones and laptops represent the traditional computing battlegrounds. The next hardware cycle involves massive unit volumes across entirely new categories. Qualcomm is positioning itself to supply the processors for nearly all of them.

The robotics sector shows this expansion clearly. Qualcomm introduced the Dragonwing IQ10 Series at CES 2026. The company designed this processor specifically as the computing core for high-performance robotics, including humanoid models and autonomous mobile robots. Qualcomm followed this launch by formalizing a long-term partnership with NEURA Robotics in March 2026. The two companies are building AI systems for robots that work safely alongside humans in factories, service industries, and homes. These automated factory arms and delivery bots process information entirely on the device without relying on remote servers.

The wearable technology market reflects the same strategy. Snapdragon chips already operate inside major wearable devices. The W5 Gen 2 processor powers the Pixel Watch 4, and the AR1 Gen 2 chip runs the Ray-Ban Meta smart glasses. Qualcomm expanded this lineup at MWC 2026 by unveiling the Snapdragon Wear Elite. This release represents the first wearable chip featuring a dedicated Hexagon neural processing unit. It can run billion-parameter AI models directly on a small device at speeds up to 10 tokens per second. That processing speed enables real-time daily logging, instant on-device transcription, and automated task execution. Samsung, Google, and Motorola have already committed to using the platform.

The augmented reality sector adds another layer of hardware demand. Snap recently signed a multi-year agreement to use Snapdragon XR chips for its upcoming consumer AR glasses. Meta and Samsung already rely on these processors. Qualcomm now supplies the hardware foundation for every major smart glasses manufacturer globally.

A specific engineering advantage connects all these product categories. Every robot vacuum, automated lawn mower, augmented reality frame, and health tracker faces the same strict physical limitation. They operate on limited battery capacity and cannot afford the energy required to ping cloud servers for every digital decision. They need maximum computing performance using the lowest possible wattage. Qualcomm spent twenty years perfecting this exact mobile architecture. The company currently dominates the market for low-power processing.

The MediaTek Roadmap for Semiconductor Re-rating

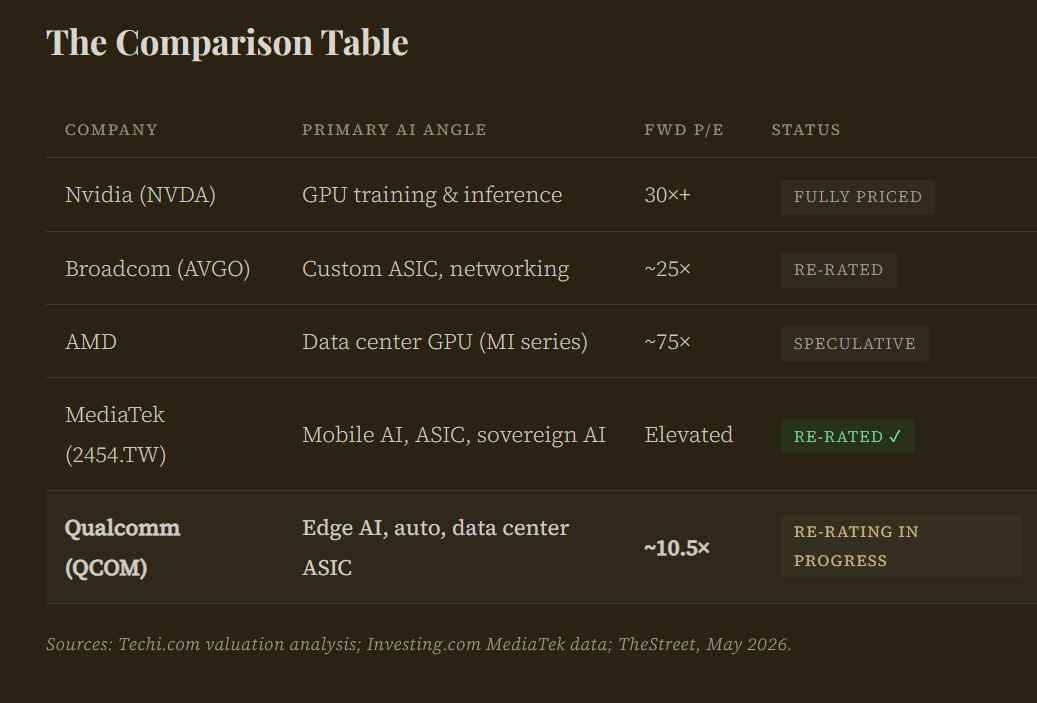

Investors looking for a historical comparison should examine MediaTek. The Taiwan-based semiconductor designer historically competed directly with Qualcomm in the mobile market. MediaTek executed a similar pivot toward artificial intelligence hardware. The market rewarded the move heavily. MediaTek stock surged from 1,130 to 4,440 Taiwan dollars over a 52-week period. That nearly fourfold increase followed new ASIC partnerships for the Nvidia GB10 program and strong demand for flagship Dimensity chips. CEO Rick Tsai guided the company into sovereign AI projects. Financial markets adjusted its valuation multiple to match the new growth profile.

Qualcomm is executing the exact same strategy. It holds deeper patent portfolios, stronger intellectual property, and a US-based balance sheet. TrendForce expects custom ASIC shipments to grow 44.6% in 2026. That is almost three times the growth rate of general-purpose GPUs. Inference tasks represent the largest ongoing cost in enterprise AI. Custom ASICs can run inference workloads at scale for 65% less money than traditional GPUs. Qualcomm built its new enterprise business to capture this exact cost-saving demand.

Hidden Value in Automotive and Executive Alignment

Financial analysts frequently ignore the automotive division when discussing Qualcomm. Yet automotive revenue reached a record $1.3 billion in Q2 FY2026. That represents a 38% year-over-year increase. Amon expects the automotive segment to exit fiscal 2026 at an annualized run rate above $6 billion. A standalone software and hardware business growing at that pace carries an enterprise value of tens of billions of dollars. The Snapdragon Digital Chassis already operates inside production vehicles for major partners like Volkswagen and Stellantis.

The valuation gap remains remarkably wide. Qualcomm trades at a forward P/E ratio of approximately 10.5x. The broader S&P 500 averages 21x. Nvidia trades well above 30x. Qualcomm generates $12.8 billion in free cash flow, buys back $20 billion in stock, and continues to grow its new enterprise segments. Melius Research raised its price target from $170 to $220 in May 2026. Analysts pointed to the data center business as a major catalyst.

(Sources: Techi.com valuation analysis; Investing.com MediaTek data; TheStreet, May 2026.)

Operational Risks and Market Headwinds

The core smartphone business still faces ongoing pressure. Global memory chip shortages are restricting smartphone manufacturing. Suppliers are currently prioritizing high-bandwidth memory for AI training servers over standard mobile memory. This dynamic is constraining handset production plans for major Chinese manufacturers. Qualcomm issued Q3 FY2026 guidance below analyst expectations. The stock dropped 7% shortly after the ByteDance rally as traders took short-term profits.

Legal and geopolitical factors also require attention. A licensing dispute with ARM Holdings heads to trial in October 2026. This creates a legal overhang for the Snapdragon product line. Serving a company like ByteDance also carries export control risks. Regulatory environments shift rapidly. Qualcomm is designing inference chips that sit right at the legal boundary of international performance caps.

Qualcomm secured a custom silicon agreement with a major cloud provider. It posted record automotive revenues. Its new edge AI processor outperforms competing Intel chips on critical efficiency metrics. The ByteDance partnership finally brings the data center narrative into public view. Management ties its own financial success almost entirely to equity performance. The company trades at half the market multiple while peers with similar transitions saw massive stock appreciation. The artificial intelligence sector is moving into a new phase defined by power efficiency and custom enterprise hardware. Qualcomm operates exactly in this space.

Disclaimer:

All views expressed are my own and are provided solely for informational and educational purposes. This is not investment, legal, tax, or accounting advice, nor a recommendation to buy or sell any security. While I aim for accuracy, I cannot guarantee completeness or timeliness of information. The strategies and securities discussed may not suit every investor; past performance does not predict future results, and all investments carry risk, including loss of principal.

I may hold, or have held, positions in any mentioned securities. Opinions herein are subject to change without notice. This material reflects my personal views and does not represent those of any employer or affiliated organization. Please conduct your own research and consult a licensed professional before making any investment decisions.