SMCI, Super Micro Computer, AI rack-scale shipper tightening its grip; AI server racks, liquid-cooled data centers

AI rack-scale shipper tightening its grip; AI server racks, liquid-cooled data centers

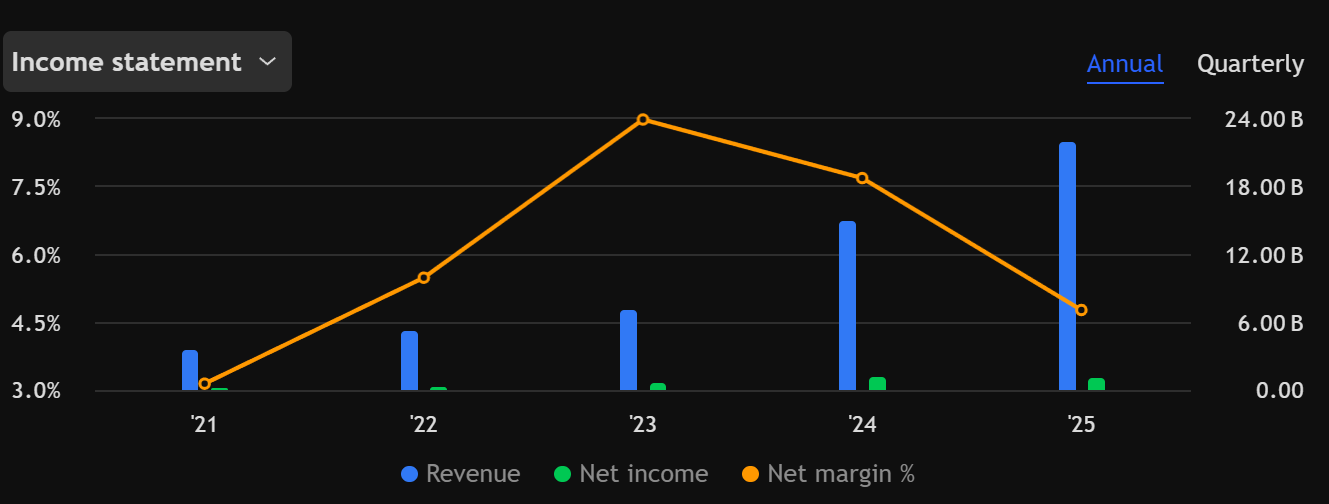

Supermicro sells the hardware that makes AI run. The company generated about $22 billion in fiscal 2025 revenue, a sharp year-over-year increase. Its bet is simple: ship complete AI racks faster than anyone else.

Latest News

On September 8, 2025, Nokia and Supermicro announced a strategic partnership to deliver integrated, AI-optimized data center networking and compute solutions, initially targeting cloud providers and carriers in Europe and North America.

The joint product is a turnkey package that combines Nokia’s data center networking with Supermicro’s rack-scale servers, sold through a shared go-to-market model. This matters because AI deployments are shifting toward pre-validated stacks, which shorten time-to-revenue for customers and reward vendors who own more of the value chain. It also gives Supermicro a higher seat at the table, selling full AI factories rather than individual servers.

Recent Earnings

Supermicro reported Q4 FY25 results, for the period ending June 30, on August 5, 2025. Revenue came in at $5.8 billion, up sequentially, with adjusted EBITDA of $339 million and operating cash flow of $864 million. Cash and equivalents stood at $5.2 billion. Management guided FY26 revenue to at least $33 billion. Results fell short of Street expectations on revenue and margins, and the stock reflected that miss.

The revenue mix continues to tilt toward AI platforms, especially full racks with liquid cooling. CEO Charles Liang credited FY25’s surge to leadership among Neoclouds, CSPs, enterprises, and sovereign buyers, expecting the count of large data center customers to rise from four to six to eight in FY26.

Management also highlighted faster deployment using its Data Center Building Block Solutions and broader global production, which helps offset tariffs and regional costs. The key near-term watchpoint is margin recovery as Blackwell systems ramp and rack-level integration gains pricing power.

Analysis and Forward Outlook

Three questions drive the stock from here.

First, supply chain and working capital. Volume growth without cash flow can strain liquidity, but Q4’s $864 million in operating cash flow and a $5.2 billion cash cushion provide breathing room as inventory turns normalize.

Second, pricing discipline versus commoditization. Sub-10 percent gross margins are acceptable during a build phase but must improve as Blackwell and the upcoming GB300 lines scale with higher attach rates of services and networking.

Third, channel reach. The Nokia partnership and similar alliances can turn one-off server bids into repeatable, full-stack wins. If Supermicro continues landing rack-scale deals with validated networking and cooling, it can regain operating leverage that was pressured during the expansion.

Guidance of $33 billion for FY26 signals confidence in backlog conversion and GPU supply. For investors, this is growth at industrial margins, powered by speed—the ability to productize new NVIDIA platforms rapidly and ship complete racks from sites in the US, the Netherlands, Taiwan, and Malaysia. If the company maintains cash generation and expands its large customer base, the multiple has room to rise even with cautious margins.

Conclusion

I am cautiously bullish. The near-term miss and margin volatility are real, yet the setup remains constructive. FY26 guidance and new partnerships point to durable demand. If Supermicro lifts margins through rack-scale mix and networking attach while keeping cash flow strong, its position in AI infrastructure will strengthen, not fade.

Disclaimer:

“All views expressed are my own and are provided solely for informational and educational purposes. This is not investment, legal, tax, or accounting advice, nor a recommendation to buy or sell any security. While I aim for accuracy, I cannot guarantee completeness or timeliness of information. The strategies and securities discussed may not suit every investor; past performance does not predict future results, and all investments carry risk, including loss of principal.

I may hold, or have held, positions in any mentioned securities. I receive no compensation for this content and do not intend to influence market prices. Opinions herein are subject to change without notice. This material reflects my personal views and does not represent those of any employer or affiliated organization. Please conduct your own research and consult a licensed professional before making any investment decisions.”

Bullish outlook