Tesla, Inc. (TSLA): Betting the Farm on Robots While Cars Stall

TSLA stands atop the electric vehicle market at extreme valuation multiples, yet much of its premium hinges on the success of future robotics and AI initiatives that remain uncertain. While Tesla, Inc. has demonstrated impressive growth in vehicle delivery and energy products, its current valuation assumes flawless execution of nascent technologies-a bet that may be too optimistic given mounting execution risks.

High-Valuation Metrics Signal Caution

Tesla, Inc.'s stock trades at a forward price-to-earnings ratio of 118.9× and a price-to-sales ratio of 8.6×, far above industry norms [1]. By comparison, the S&P 500's average forward P/E is around 18×, and traditional automakers like Ford and GM hover below 10× [1]. In simple mathematical terms, TSLA must multiply its earnings by over 6× just to align with the broader market's valuation, implying the market expects exponential profit growth primarily from non-automotive ventures.

Robotics: A Future on Shaky Wheels

Much of Tesla, Inc.'s envisioned upside lies in its robotaxi and humanoid robotics ambitions. The upcoming robotaxi service in Austin, Texas, is slated for launch this month, yet Q1 deliveries fell 13% year-over-year and operating profit plunged 66% to $399 million [2]. Even if regulatory hurdles are cleared, scaling an autonomous fleet to meaningful revenue levels will require massive capital and flawless software-no small feat given the complexities of real-world driving [2].

Global EV Competition Intensifies

On the global stage, Tesla, Inc. is contending with rapidly advancing Chinese EV makers. In May 2025, BYD alone delivered over 376,930 vehicles in China (up 40%), and the combined sales of Li Auto, XPeng, and NIO topped 97,612 units-a 50% increase versus last year-while Tesla's Chinese deliveries dropped 6% [3]. These competitors benefit from aggressive pricing, government support, and expanding product lineups, eroding the market share that Tesla once enjoyed.

AI Infrastructure: A Fierce Arena

Tesla, Inc.'s AI ambitions extend beyond autonomous vehicles into custom chips and its Dojo supercomputer, but it faces heavyweight rivals. Meta Platforms plans to invest $65 billion in AI infrastructure this year, while global tech giants will pour $320 billion into AI and data centers in 2025 [4][5]. Meanwhile, the competition on foundation models is a "triathlon" of model development, customer adoption, and costly infrastructure build-out-no single player can win all three [6]. Without a clear moat, Tesla's AI edge may be fleeting against hyperscalers with deeper pockets.

Half-Value Hypothesis: The Path to Reality

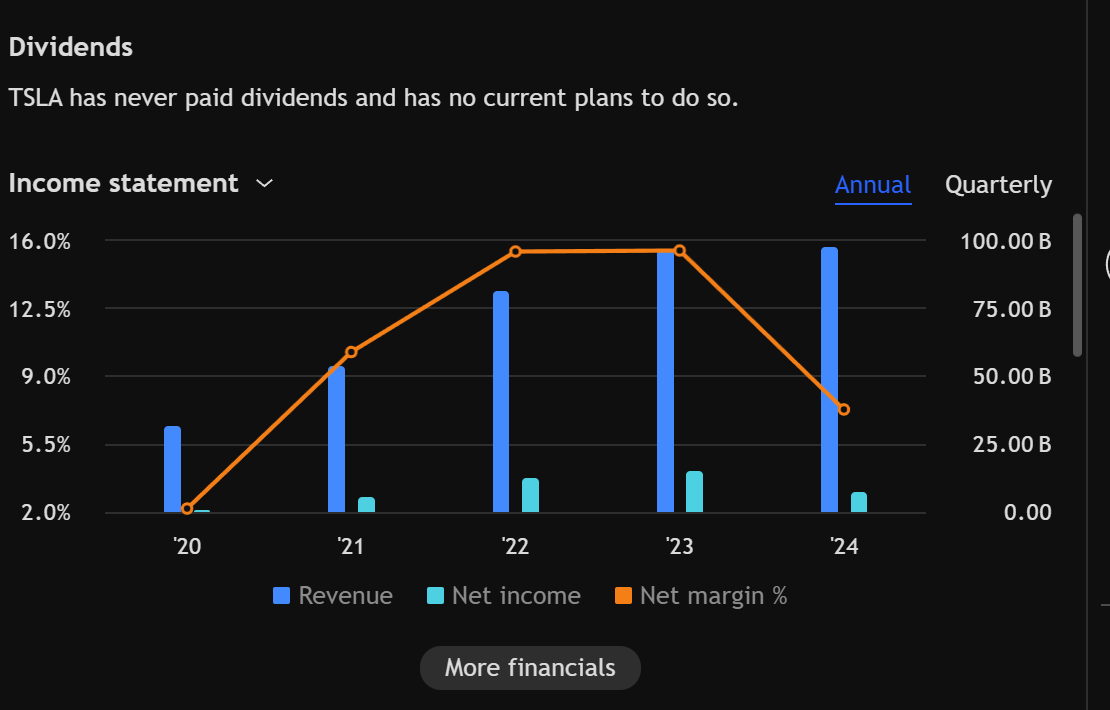

Given these execution uncertainties and the stretched base required for future earnings, a valuation reset seems plausible. If TSLA's future profits from robotics and AI fall short by even 50% of market expectations, the share price could likewise retrace by half. Tesla, Inc.'s Q1 results-$19.3 billion in revenue (down 9%) and $409 million net income (down 71%)-underscore how far the business can underperform relative to lofty forecasts before investor sentiment sours completely [7]. A more conservative multiple of 60× forward earnings would align TSLA with high-growth peers, cutting the current valuation nearly in half.

Disclaimer:

All views expressed are my own and are provided solely for informational and educational purposes. This is not investment, legal, tax, or accounting advice, nor a recommendation to buy or sell any security. While I aim for accuracy, I cannot guarantee completeness or timeliness of information. The strategies and securities discussed may not suit every investor; past performance does not predict future results, and all investments carry risk, including loss of principal.

I may hold, or have held, positions in any mentioned securities. I receive no compensation for this content and do not intend to influence market prices. Opinions herein are subject to change without notice. This material reflects my personal views and does not represent those of any employer or affiliated organization. Please conduct your own research and consult a licensed professional before making any investment decisions.

Bullish outlook.

Tags: TSLA, TSLA 0.00%↑

References

[1] "Tesla's stock is too expensive-even if Musk and Trump make up," MarketWatch, Jun. 2025. https://www.marketwatch.com/story/teslas-stock-is-too-expensive-even-if-musk-and-trump-make-up-7cd5f65d

[2] "Tesla Stock Is Falling. Is It a 'Sell the News' Month?" Barron's, Jun. 2025. https://www.barrons.com/articles/tesla-stock-robotaxi-ai-sell-e69bb7dc

[3] "Chinese EV Makers Pull Away From Tesla With Sales Gains," Barron's, Jun. 2025. https://www.barrons.com/articles/chinese-ev-makers-tesla-sales-4da484e4

[4] "Meta plans investments into AI-driven humanoid robots, memo shows," Reuters, Feb. 14 2025. https://www.reuters.com/technology/artificial-intelligence/meta-plans-investments-into-ai-driven-humanoid-robots-memo-shows-2025-02-14/

[5] "Meta Platforms to Invest $65 Billion in AI Infrastructure Amid Growing Competition," ODSC, Jan. 24 2025. https://opendatascience.com/meta-platforms-to-invest-65-billion-in-ai-infrastructure-amid-growing-competition/

[6] "AI companies' triathlon: Who's leading in models, users and infrastructure," Axios, Nov. 27 2024. https://www.axios.com/2024/11/27/ai-race-openai-google-meta-anthropic

[7] "Elon Musk to pull back in Doge role starting May amid 71% dip in Tesla profits," The Guardian, Apr. 22 2025. https://www.theguardian.com/technology/2025/apr/22/tesla-sales-musk-white-house-exit