Why Grab (GRAB) Might Be One of Southeast Asia’s Next Breakout Tech Plays

Grab Holdings Inc. (GRAB), the Southeast Asian super-app that spans ride-hailing, food delivery, and financial services, has quietly been threading together enough momentum that it is worth a fresh look.

1. Latest Moves: Partnerships, Products, and Platform Leverage

Grab’s strategy in 2025 revolves less around splashy headlines and more around layering capabilities that can become independent profit engines. One standout is its in-house mapping solution, GrabMaps, which is now being pitched beyond Southeast Asia. The company recently struck a deal to map Mongolia with local partner Tino, marking its first full-country deployment outside its home region. This signals Grab sees mapping not just as infrastructure but as a monetizable platform.

Elsewhere, Grab has doubled down on AI for merchant and driver tools. It introduced an AI Merchant Assistant and AI Driver Companion, developed in collaboration with OpenAI and Anthropic, to provide analytics, routing, voice reporting, and demand prediction. The logic is clear: embed AI into the operating fabric so that optimization, predictive insights, and automation reduce friction and cost across the ecosystem.

Remember: the classic “super-app” model works best when its components cross-feed each other. Every extra minute a user spends in the app, whether ordering, paying, riding, or banking, strengthens network effects.

The risk is that these platform-style moves may take time and upfront investment. But if Grab can convert core infrastructure into enterprise-grade services, you get optionality beyond Southeast Asia ride and delivery.

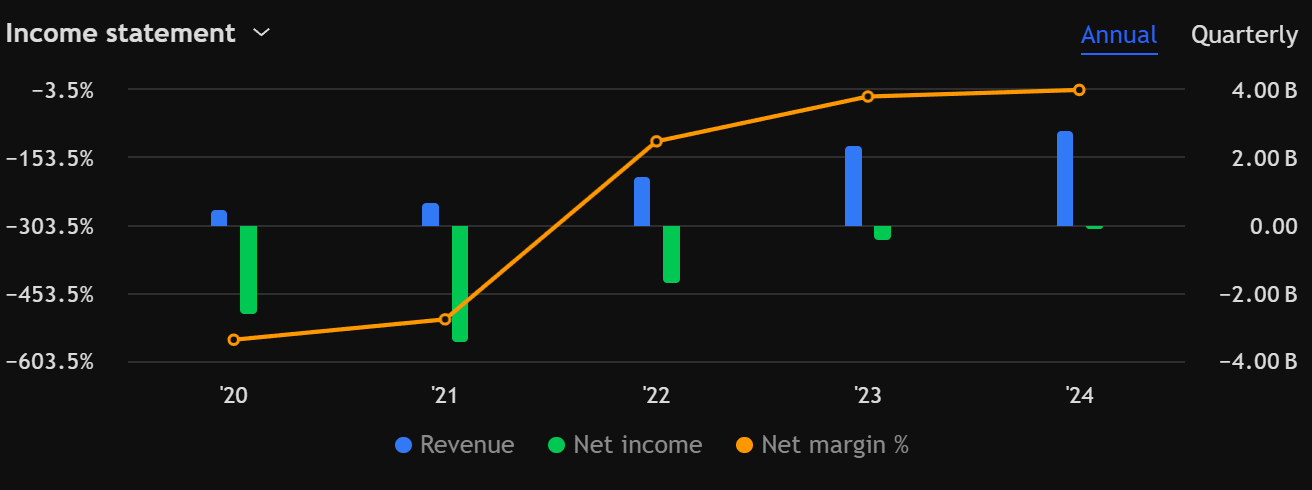

2. Recent Earnings: Turning Profitable (Sort of)

Grab’s Q2 2025 results showed real signs of breathing room. Revenue reached US $819 million, up about 23 percent year-over-year (19 percent on a constant currency basis), beating estimates. On-demand GMV rose around 21 percent to $5.4 billion. Impressively, Grab posted US $20 million in profit, turning around from a loss in the same period last year. Their adjusted EBITDA hit a record $109 million, improving by $45 million year-over-year. On a trailing 12-month basis, adjusted free cash flow was $229 million.

That said, growth is uneven across segments. Financial Services (lending, digibank) is still operating at a loss, and Grab expects segment breakeven by H2 2026. Operating cash flow for the quarter was only $64 million, offset by outflows tied to their banking and lending arms.

Furthermore, Grab has raised US $1.5 billion via a zero-coupon convertible note to buttress liquidity and maintain flexibility. They also spent approximately $274 million repurchasing 58 million Class A shares in Q2.

Past quarters were not as clean. Q4 2024’s revenue was $764 million with $11 million in net income, but guidance and EBITDA estimates disappointed the market. Full-year revenue guidance was set at $3.33–$3.40 billion, slightly below consensus.

Bottom line: Grab is crossing into profitability in spurts, but capital is still bleeding into financial services and new infrastructure.

3. Forward Outlook: Why This Could Be More Than a Ride and Delivery Story

The most compelling bull case for Grab is not just that it competes in food and transport. It is that it is trying to become the infrastructure of Southeast Asia’s digital economy.

Mainstream adoption is already here. Over 46 million monthly transacting users power Grab’s ecosystem. As urbanization and smartphone penetration deepen, Grab’s addressable base still has room to grow.

Platform optionality matters. GrabMaps, AI tools for merchants and drivers, advertising for merchants — each has margin potential beyond transaction fees. With autonomy, smart cities, logistics, and digital mapping, Grab has exposure to infrastructure markets that remain underdeveloped.

If Grab sustains consistent profitability, it could join indices or gain more institutional share, particularly among funds looking for Asia tech exposure. That would create a sustained inflow over time. It is not there yet, and valuation remains elevated, but the narrative supports it.

Risks are real but manageable. Competitive pressures from GoTo, Foodpanda, and local players remain intense. Macro weakness in Southeast Asia, including inflation and consumer pullback, could dent GMV growth. Incentive spending and regulatory risk in financial services and ride-hailing are also factors.

Valuation stretch is significant. In Q2, EPS of $0.01 met expectations, but Grab trades at high multiples relative to current earnings. Investors are pricing in high growth and optionality. If any leg stumbles, it will magnify downside.

Conclusion

I lean bullish. Grab is transitioning from unit-economics hunts to optionality bets. If it successfully converts infrastructure into revenue pillars and holds GMV growth without catastrophic margin loss, the upside is compelling. The next 12–24 months will be a make-or-break window. Either they prove profitability at scale or become just another overvalued growth name.

Disclaimer:

“All views expressed are my own and are provided solely for informational and educational purposes. This is not investment, legal, tax, or accounting advice, nor a recommendation to buy or sell any security. While I aim for accuracy, I cannot guarantee completeness or timeliness of information. The strategies and securities discussed may not suit every investor; past performance does not predict future results, and all investments carry risk, including loss of principal.

I may hold, or have held, positions in any mentioned securities. I receive no compensation for this content and do not intend to influence market prices. Opinions herein are subject to change without notice. This material reflects my personal views and does not represent those of any employer or affiliated organization. Please conduct your own research and consult a licensed professional before making any investment decisions.”

Bullish outlook

GRAB and GRAB 0.00%↑